Best Personal Loan Companies with the Lowest Rates in December 2025

We’ve named SoFi the best personal loan lender overall — it has fast funding and lets you skip upfront fees

- Winner: is LendingTree’s pick for the best personal loan company in December 2025.

- Why we like it: offers some of the fastest funding on the market and lets you skip upfront fees (they’re optional).

- Runners-up: and . Both offer low rates and unique perks that make them strong alternatives and top LendingTree picks.

Top 10 best personal loan companies

| Lender | User rating | Best for | APR | |

|---|---|---|---|---|

|

|

Big loans and no fees | 6.40% – 25.29% (with discounts) |

| Lender |

|

|---|---|

| User rating | |

| Best for | Big loans and no fees |

| APR | |

What is the best personal loan company right now?

For December 2025, is the best personal loan company according to our methodology because it offers quick funding, optional fees and competitive rates.

Other top personal loan companies include (low rates and accessible to people with fair credit) and (low rates and no fees).

LendingTree personal loan experts hand-select each of our top lenders and evaluate them for how easy they are to qualify for, cost and ease of repayment — the factors that matter most to you. Learn more about how we rate lenders.

How LendingTree works

You’d shop around for flights. Why not your loan? LendingTree makes it easy. Fill out one form and get lenders from the country’s largest network to compete for your business.

1. Tell us what you need

Take two minutes to tell us who you are and how much money you need. It’s free, simple and secure.

2. Shop your offers

LendingTree users who get at least one offer receive 20 personal loan offers on average. Compare your offers side by side to get the best deal.

3. Get your money

Pick a lender and sign your loan paperwork. You could see money in your account in as soon as 24 hours.

Best personal loan companies

Best for: Big loans and no fees – LightStream

- APR (with discounts)

- 6.40% – 25.29%

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Praesent auctor magna eu enim fringilla, eget lobortis mi cursus. Proin accumsan feugiat augue non consectetur. Phasellus tempor lectus magna, vel sagittis lorem tristique et. Nulla vulputate sollicitudin venenatis. In hac habitasse platea dictumst. Etiam varius velit tellus, et sagittis erat consequat ut. Morbi ut dui nec felis rhoncus feugiat. Duis non ante in nibh tincidunt porttitor. Phasellus sed metus nunc. Aenean faucibus elementum libero eu mollis.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Praesent auctor magna eu enim fringilla, eget lobortis mi cursus. Proin accumsan feugiat augue non consectetur. Phasellus tempor lectus magna, vel sagittis lorem tristique et. Nulla vulputate sollicitudin venenatis. In hac habitasse platea dictumst. Etiam varius velit tellus, et sagittis erat consequat ut. Morbi ut dui nec felis rhoncus feugiat. Duis non ante in nibh tincidunt porttitor. Phasellus sed metus nunc. Aenean faucibus elementum libero eu mollis.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Praesent auctor magna eu enim fringilla, eget lobortis mi cursus. Proin accumsan feugiat augue non consectetur. Phasellus tempor lectus magna, vel sagittis lorem tristique et. Nulla vulputate sollicitudin venenatis. In hac habitasse platea dictumst. Etiam varius velit tellus, et sagittis erat consequat ut. Morbi ut dui nec felis rhoncus feugiat. Duis non ante in nibh tincidunt porttitor. Phasellus sed metus nunc. Aenean faucibus elementum libero eu mollis.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Praesent auctor magna eu enim fringilla, eget lobortis mi cursus. Proin accumsan feugiat augue non consectetur. Phasellus tempor lectus magna, vel sagittis lorem tristique et. Nulla vulputate sollicitudin venenatis. In hac habitasse platea dictumst. Etiam varius velit tellus, et sagittis erat consequat ut. Morbi ut dui nec felis rhoncus feugiat. Duis non ante in nibh tincidunt porttitor. Phasellus sed metus nunc. Aenean faucibus elementum libero eu mollis.

- Get money as soon as the same day

- No fees

- Borrow up to Not specified (most lenders only offer up to $50,000)

- 0.50% autopay discount

- Checking rates will require a hard credit pull (and knock a few points off your score)

- Can’t use money for school or business expenses

- Must have good or excellent credit to qualify

I started the application process with LightStream using my real information. Here’s what I found:

- Application experience: LightStream’s application has more questions than usual because you’re getting real rates rather than estimates from prequalified offers. You’ll also have to create an account to see rates. That said, I love how straightforward LightStream’s application is — it anticipates and answers common questions.

- Unusual questions to prepare for: Time at current address, time with current employer, estimated home equity, checking and savings balances plus stocks and bonds, retirement assets

LightStream is one of the few personal loan lenders that offers more than $50,000, making its loans ideal for big expenses. Its competitive rates and low fees could translate to huge savings if you need a large loan.

Unlike many personal loan companies, LightStream doesn’t let you check your rates by prequalifying. If you want to see your rates and terms, LightStream will do a hard credit pull, which will cause your credit score to take a small, temporary dip.

While LightStream offers loans up to Not specified, LendingTree marketplace customers may not receive offers at this maximum loan amount.

LightStream doesn’t specify its exact credit score requirements, but you must have good to excellent credit to qualify. Most of the applicants that LightStream approves have the following in common:

- At least five years of on-time payments under a variety of accounts (credit cards, auto loans, etc.)

- Stable income and the ability to handle paying their current debt obligations

- Savings, whether in a bank account, an investment account or a retirement account

What is a personal loan?

A personal loan gives you a lump sum of money that you’ll pay back in equal monthly payments. The lender will usually send the money straight to your bank account — sometimes as soon as the same day.

What else to know:

-

Fixed interest

Interest stays the same during the loan, and so do your payments. Credit card interest goes up and down with the market. -

How to qualify

There’s no universal minimum credit score for personal loans — but the better your credit, the cheaper your loan will likely be. Learn more about personal loan requirements. -

How to apply

You can apply for a personal loan on the lender’s website or use a service like LendingTree to get quotes from up to five lenders at once.

Personal loans are a popular solution for dealing with debt. Nearly three quarters (72%) of Americans have a personal loan, have had one in the past or have considered getting one, according to a LendingTree survey.

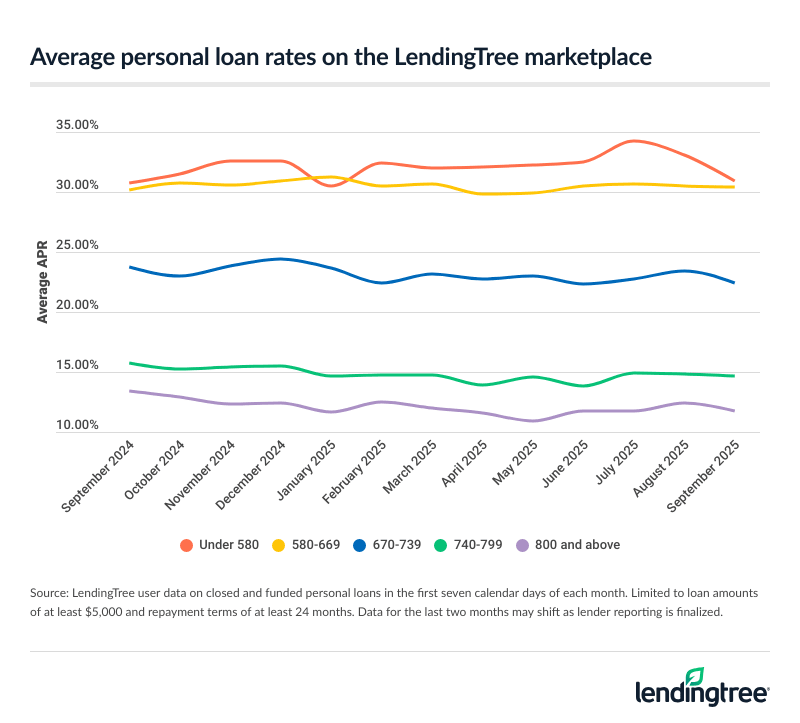

Personal loan rates

We’ve compiled the average personal loan rates for LendingTree marketplace users so you can estimate the rates you’ll likely qualify for based on your credit score.

| Credit tier | Average APR |

|---|---|

| Excellent (800 and above) | 11.66% |

| Very good (740-799) | 14.35% |

| Good (670-739) | 22.83% |

| Fair (580-669) | 30.22% |

| Poor (under 580) | 32.09% |

Track personal loan rates with LendingTree

Personal loan rates have held steady over the past year, but they remain relatively high — making it more important than ever to compare lenders and find the best offer for your credit profile.

{kind=link}

Calculate your loan payments

How much will your loan cost?

It’s hard to know how much your loan will actually cost when you’re looking at broad APR ranges. We’ll walk you through how to estimate the cost of your loan in dollars and cents.

Let’s assume you borrow $5,000 over a loan term of 48 months. Let’s also assume your loan has no fees. Here’s a quick estimate of the cost of your loan in dollars and cents.

| Credit score range | Average APR | Monthly payment | Interest | Total cost |

|---|---|---|---|---|

| Excellent (800 and above) | 11.66% | $130.84 | $1,280.13 | $6,280.13 |

| Very good (740-799) | 14.35% | $137.51 | $1,600.57 | $6,600.57 |

| Good (670-739) | 22.83% | $159.79 | $2,670.02 | $7,670.02 |

| Fair (580-669) | 30.22% | $180.67 | $3,672.17 | $8,672.17 |

| Poor (under 580) | 32.09% | $186.16 | $3,935.60 | $8,935.60 |

Improving your credit before getting a loan will help you get lower rates and save money. You could save more than $1,804 on your loan by raising your score from “fair” to “very good.”

How to choose the best loan

Once you have loan offers, use our loan calculator to compare APRs, monthly payment and total interest payments. Here’s what to expect and watch out for based on your credit score:

| Your credit band | Probable offers | Tips |

|---|---|---|

| Excellent (800 and above) | Low rates, options with no fees | Prioritize offers with low rates and no origination fee. |

| Good to very good (670-799) | Slightly higher rates, may need to pay fees | Lenders deduct origination fees before sending your loan, so make sure you’ll get the full amount of money you need. |

| Fair (580-669) | Fewer options with higher rates, fees likely | Find the offer with the lowest APR that has a monthly payment you can afford. |

| Poor (under 580) | Few options, highest rates | Add a co-borrower or collateral for lower rates and better odds of approval. |

Expert insights on finding the lowest personal loan rate

If you don’t shop around for the best rate on your next personal loan, you’re probably going to pay too much. Rates, terms and amounts can vary significantly by lender, so it is absolutely worth the effort to compare offers from multiple personal loan companies.

Life’s too expensive today to settle for paying more than you need.

Best loan companies for every need

Frequently asked questions

Of our top picks for December 2025, offers the lowest starting rate ( APR) for secured personal loans, and LightStream offers the next-lowest starting rate (6.40% APR with autopay) for unsecured loans.

LendingTree’s top 10 lenders offer safe personal loans that you can apply for online. Read about personal loan disadvantages to protect yourself from the risks that come with any personal loan.

Choosing the right personal loan lender is all about shopping around. Prequalify with several lenders, compare your offers and choose the one that fits your budget. You can get offers from up to five lenders at once with LendingTree.

Online-only lenders typically offer fast funding and can be easier to qualify for than traditional personal loans from brick and mortar banks, but they sometimes come with one-time origination fees that can make your loan more expensive.

Yes, some personal loan comparison sites are trustworthy. LendingTree writers and editors evaluate lenders impartially and don’t receive compensation for their reviews. Learn more about how we review lenders.

Our methodology

We reviewed more than 30 lenders that offer personal loans to determine the overall best 10 lenders by these metrics. According to our systematic rating and review process, the best personal loans come from SoFi, Upgrade, Best Egg, Discover, LendingClub, LightStream, PenFed, Prosper, Rocket Loans and Upstart. LendingTree reviews and fact-checks our top lender picks on a monthly basis.

Accessibility. We look for lenders with fewer barriers to approval and award points for lower credit requirements, nationwide access, fast funding and simple applications.

Rates and terms. We prioritize lenders that offer low starting rates, minimal fees, flexible terms and APR discount opportunities.

Repayment experience. We choose lenders with strong reputations, convenient self-service tools, responsive support and borrower-friendly perks.

Why trust our methodology?

Our writers and editors dig through the facts, contact lenders directly and even go through the application process ourselves if it helps better explain what you can expect. As a Certified Financial Education Instructor℠, I’m committed to breaking down complex financial details so people can make confident, informed decisions with their money.

Jessica’s experience in editing and financial education helps shape LendingTree articles that are clear, accurate and truly useful to readers. Her certification means our recommendations are built on a foundation of consumer-first financial knowledge — not just numbers.