Can I Lower My Mortgage Interest Rate Without Refinancing?

Not everyone can or even desires to go through the process of replacing their current home loan. As a borrower you may wonder, “Can I lower my mortgage interest rate without refinancing?”

The short answer is yes, though your options are very limited. You may qualify for a mortgage rate reduction, if you’re facing financial turmoil. But in most cases, you’ll either need to take another route to cut your mortgage costs or work toward getting a refinance approval.

Can I lower my mortgage rate without refinancing?

Your mortgage interest rate plays a major part in determining how affordable your loan is, and the easiest way to trade a higher rate for a lower one is through a mortgage refinance.

There is one way you can get a lower mortgage interest rate without refinancing, however. A mortgage modification allows you to change the original terms of your home loan due to a financial hardship.

Your lender may adjust your loan by:

- Extending your loan term

- Reducing your principal balance

- Lowering your mortgage rate

Not every borrower can get a loan modification, though. Typically, you must either be behind on your mortgage or anticipate that you’ll miss your upcoming monthly mortgage payments.

This option should only be pursued in dire situations, though, since there are significant risks that come with it. You’ll likely have to prove financial stress, even to the point that you make late mortgage payments, which will drop your credit score.

Falling just 30 days behind on your mortgage payments can drop your credit score by as many as 110 points, according to FICO research.

Why mortgage rates matter

Your mortgage rate represents the cost of borrowing money to buy a home, and it’s expressed as a percentage of the loan amount. Mortgage rates have a major influence on a home loan’s affordability.

Here’s an example: Let’s say you’re quoted a 5% interest rate on a 30-year mortgage for a $300,000 home and you’re making a 20% down payment ($60,000). The principal and interest portion of your monthly payment would be approximately $1,289.

If you take that same loan but increase the interest rate to 6%, your estimated principal and interest payment would jump to $1,439 — a monthly difference of $150, and a more than $54,000 difference in interest over the life of the loan.

How your mortgage rate is determined

Several factors help determine the mortgage rate you’re offered, including:

- Your credit score. The higher your score, the lower your rate will be.

- Your down payment amount. The larger your down payment, the lower your rate tends to be.

- Your mortgage amount. Larger loans often qualify for lower interest rates than smaller ones.

- Your repayment term. Shorter-term loans, like a 15-year mortgage, tend to have lower rates.

- Your mortgage program. Conventional loans will have varying rates compared with FHA or VA loans, for example.

- Your interest rate type. Fixed-rate loans tend to have higher rates than variable-rate loans — but you get the security of a rate that never changes.

- Your home’s location. The mortgage market can be highly localized, and rates in one town may be different from those in another.

- Your mortgage points. Mortgage points are essentially an optional, upfront fee you pay to get a lower rate.

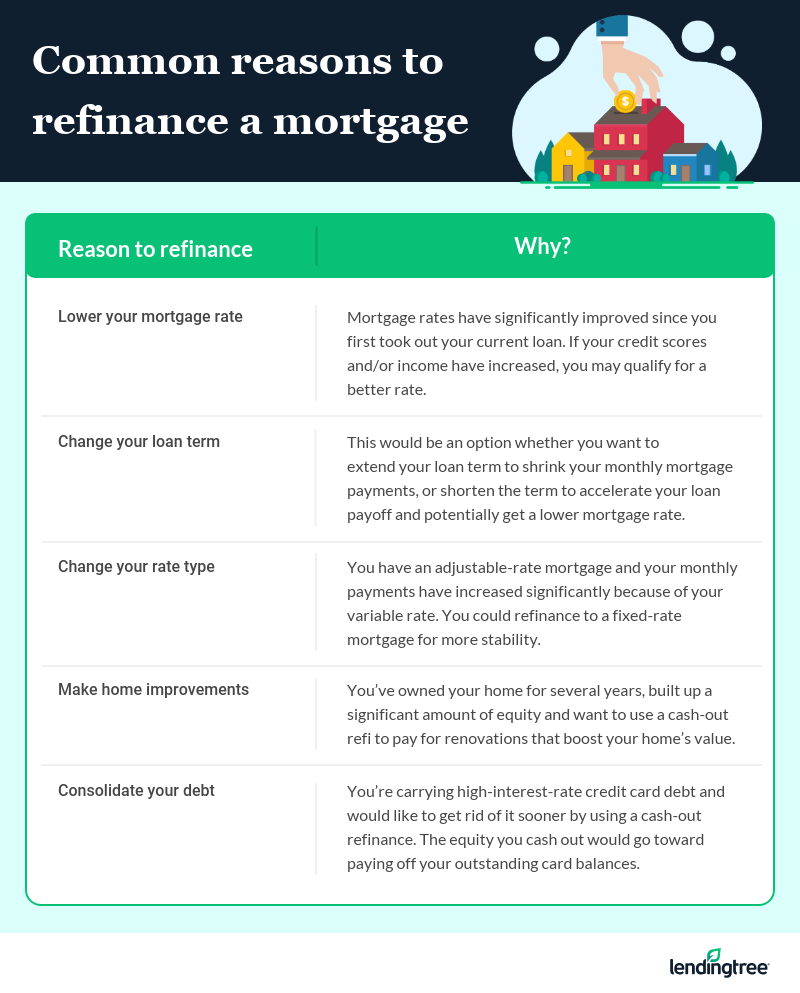

Reasons mortgage borrowers refinance their loans

Since it’s next to impossible to lower your mortgage rate without refinancing, you might be considering whether a mortgage refinance is worth your time and money.

Refinancing your mortgage can serve a variety of needs, and not all borrowers refinance for the same purpose. Here are some common reasons to refi and scenarios when they might make sense for you:

Alternative ways to save money on your mortgage

If a refinance doesn’t fit into your short-term financial goals, there are other methods you can use to save money on your mortgage. Here are some alternative ways to lower your house payment without refinancing:

Recast your mortgage

A mortgage recast lowers your monthly mortgage payments. You pay a lump sum of cash to your lender, which is applied to your outstanding principal balance. Your lender then recalculates your monthly payments based on the reduced balance amount. Your loan repayment term and interest rate won’t change, however.

You may need a minimum lump sum amount of $5,000 to $10,000, and also might have to pay a recasting fee. Check with your lender for specific requirements.

Drop mortgage insurance

If you used a conventional loan to buy your home and put down less than 20%, chances are you have private mortgage insurance (PMI) — this increases your monthly mortgage payment amount. Once you’ve built 20% equity in your home, request that your lender remove PMI from your loan, which would lower your monthly payment amount.

Things are a bit more complicated if you have an FHA loan, as FHA mortgage insurance premiums are harder to drop. To get rid of FHA mortgage insurance, you’ll need to put down at least 10% at closing and wait 11 years. Otherwise, the only way to drop the insurance is by refinancing into a conventional mortgage — after you have at least 20% equity.

Make biweekly payments

It’s more of a long game, but splitting your mortgage payments in half and making biweekly payments can save you money and eventually shorten your loan term.

Over the course of a year, you’d make 26 biweekly payments, which works out to 13 full payments. If you start biweekly payments when you first borrow your mortgage and continue them throughout your loan term, you’d end up shaving off more than four years from your repayment period.