Most Popular Metros for Gen Z Homebuyers

Though many Generation Zers born between 1997 and 2012 are children or young teens, some older members are attending college, starting careers and buying homes for the first time.

But where are Gen Zers looking to buy? To answer, LendingTree analyzed mortgage purchase requests from adult Gen Z users of the LendingTree platform across the nation’s 50 largest metros from Jan. 1 through Dec. 31, 2022.

Although adult Gen Zers (ages 18 to 25) account for an average of 14.91% of potential homebuyers across the nation’s 50 largest metros, that figure will likely grow over the coming years.

On this page

Key findings

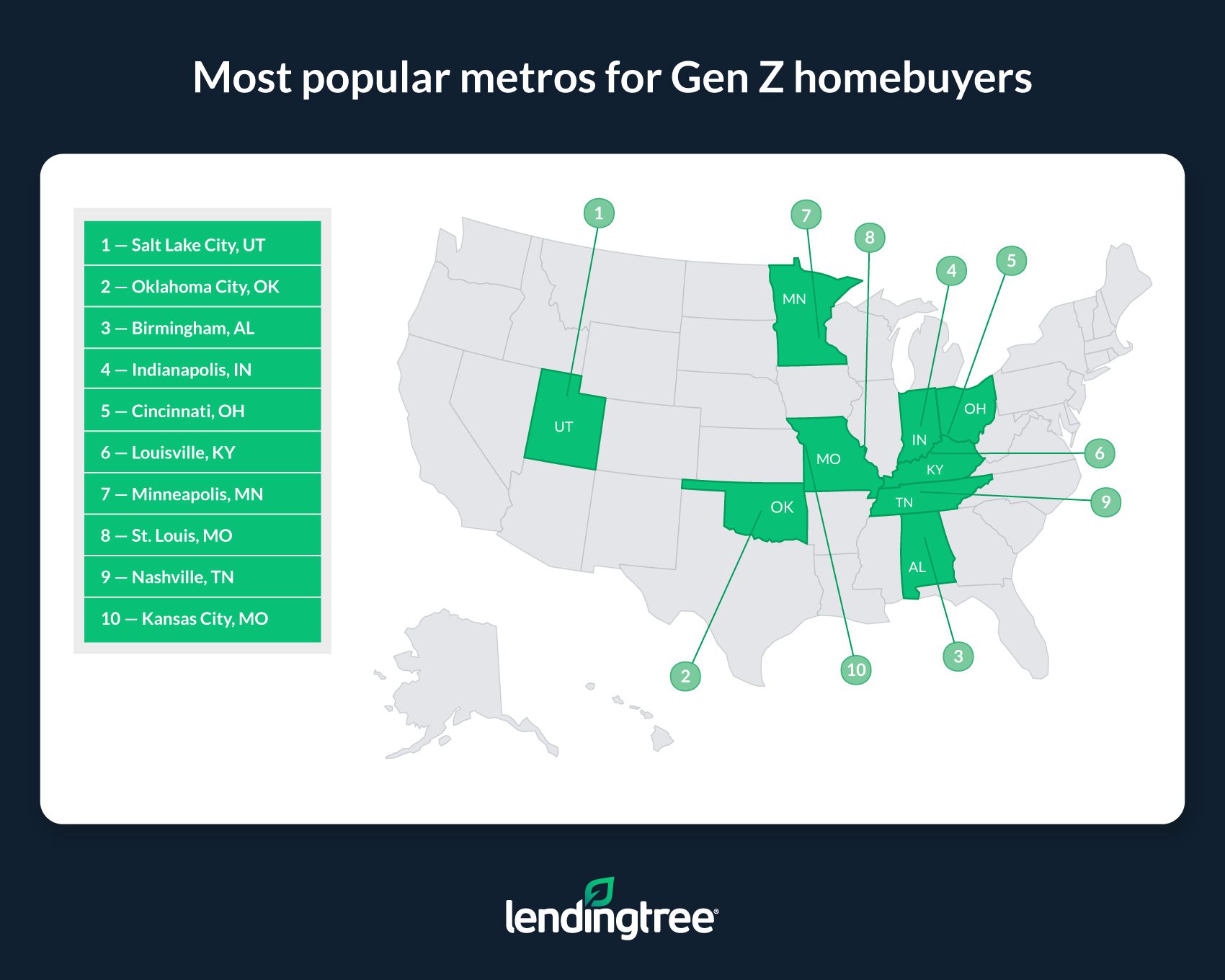

- At 22.59%, Salt Lake City has the largest share of mortgage requests from Gen Zers. Though the average mortgage amount in Salt Lake City is higher than in many of the nation’s other large metros, it’s a hot spot for younger homebuyers, likely owing to — among other factors — its strong jobs market and a good blend of urban and rural amenities.

- After Salt Lake City, relatively inexpensive Oklahoma City and Birmingham, Ala., are the next most popular metros among Gen Z buyers. Respectively, 22.36% and 20.79% of mortgage requests in these two metros come from Gen Zers.

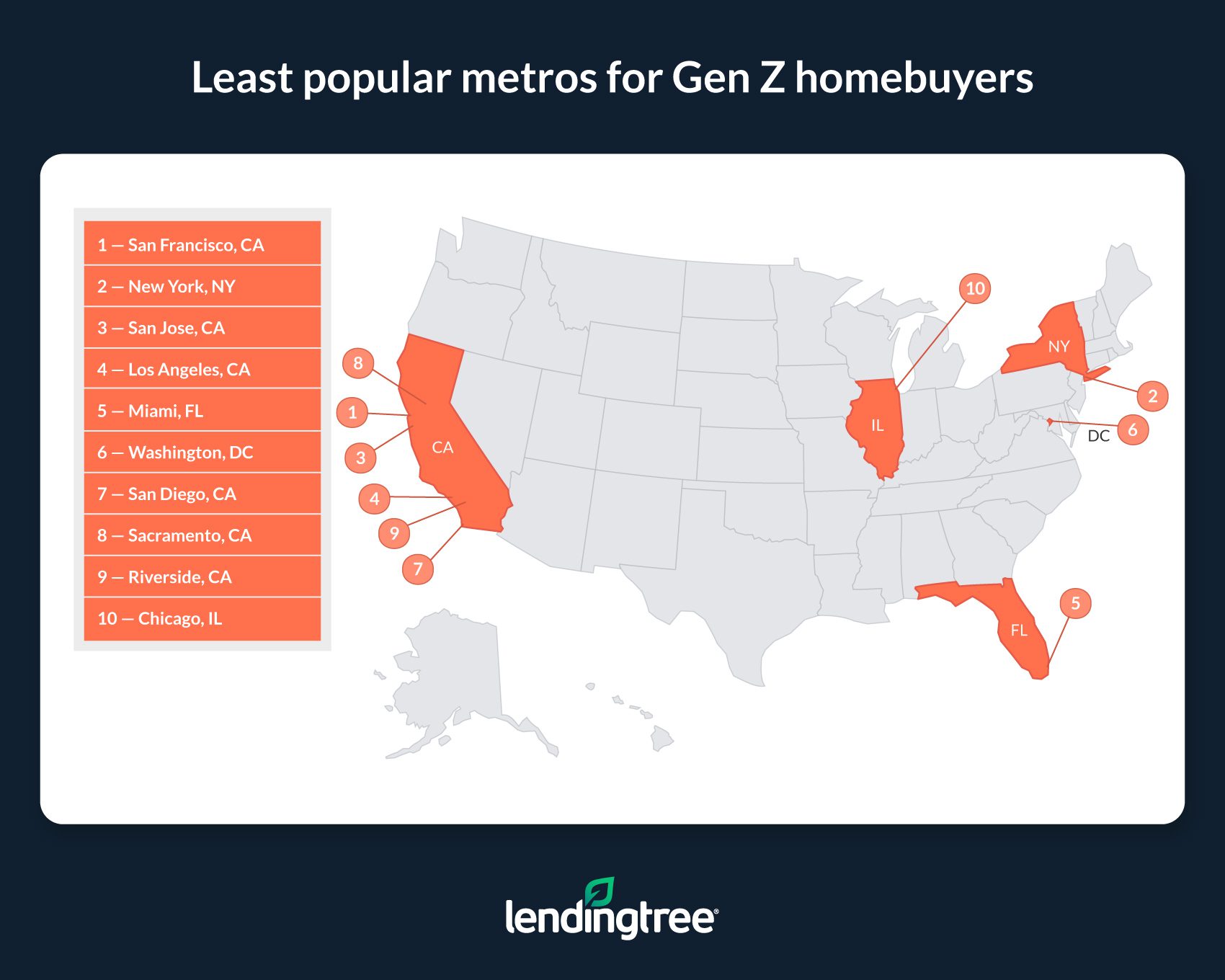

- In expensive San Francisco, New York and San Jose, Calif., the smallest percentage of mortgages are being requested by Gen Zers. Respectively, 7.76%, 8.88% and 9.70% of mortgage requests in these metros come from Gen Zers. While these shares are lower than the 50-metro average of 14.91%, they’re still nothing to sneeze at. As Gen Zers age over the coming years, these shares will likely rise even higher.

- All in all, six of the 10 least popular metros for potential Gen Z buyers are in California. This shows how much of an obstacle the state’s expensive real estate can be for younger buyers to overcome.

- The average credit score of Gen Z mortgage borrowers can vary widely across the U.S. The average credit score among Gen Zers who made mortgage purchase requests is highest in Buffalo, N.Y., at 707 — 56 points above the average score of 651 in New Orleans, where it’s the lowest.

- Down payment amounts also vary by metro. There’s a $59,034 difference between the average down payment among potential Gen Z homebuyers of $77,786 in San Jose and $18,752 in Oklahoma City — the highest and the lowest across the 50 largest metros.

- Like credit scores and down payments, mortgage amounts can change quite a bit depending on where buyers live. In San Jose, the average mortgage amount offered to Gen Zers is $541,436. That’s $347,836 more than the $193,600 average in Cleveland, where potential Gen Z homebuyers borrow the least.

Most popular metros for Gen Z homebuyers

No. 1: Salt Lake City

- Share of mortgage requests from Gen Zers: 22.59%

- Average Gen Z homebuyer age: 22

- Average credit score among potential Gen Z homebuyers: 678

- Average down payment amount among potential Gen Z homebuyers: $30,456

- Average requested loan amount among potential Gen Z homebuyers: $340,484

No. 2: Oklahoma City

- Share of mortgage requests from Gen Zers: 22.36%

- Average Gen Z homebuyer age: 22

- Average credit score among potential Gen Z homebuyers: 680

- Average down payment amount among potential Gen Z homebuyers: $18,752

- Average requested loan amount among potential Gen Z homebuyers: $208,475

No. 3: Birmingham, Ala.

- Share of mortgage requests from Gen Zers: 20.79%

- Average Gen Z homebuyer age: 22

- Average credit score among potential Gen Z homebuyers: 679

- Average down payment amount among potential Gen Z homebuyers: $22,024

- Average requested loan amount among potential Gen Z homebuyers: $215,894

Least popular metros for Gen Z homebuyers

No. 1: San Francisco

- Share of mortgage requests from Gen Zers: 7.76%

- Average Gen Z homebuyer age: 23

- Average credit score among potential Gen Z homebuyers: 674

- Average down payment amount among potential Gen Z homebuyers: $66,561

- Average requested loan amount among potential Gen Z homebuyers: $531,089

No. 2: New York

- Share of mortgage requests from Gen Zers: 8.88%

- Average Gen Z homebuyer age: 23

- Average credit score among potential Gen Z homebuyers: 697

- Average down payment amount among potential Gen Z homebuyers: $46,476

- Average requested loan amount among potential Gen Z homebuyers: $340,501

No. 3: San Jose, Calif.

- Share of mortgage requests from Gen Zers: 9.70%

- Average Gen Z homebuyer age: 23

- Average credit score among potential Gen Z homebuyers: 683

- Average down payment amount among potential Gen Z homebuyers: $77,786

- Average requested loan amount among potential Gen Z homebuyers: $541,436

What’s in store for Gen Z buyers in 2023 and beyond

Our findings illustrate that Gen Zers make up a noteworthy share of homebuyers in many of the nation’s largest metros. While this doesn’t undercut how difficult it can be to buy a home — especially for younger buyers without as much cash or experience in the housing market — it helps dispel the myth that homeownership is impossible for all young Americans.

Owing to these challenges, cheaper alternatives to buying, like renting or living with family, may remain the best option for many members of Generation Z.

Fortunately, while these more affordable options might be more attainable for now, Gen Zers will likely have plenty of opportunities to become homebuyers over the coming years as their earnings increase. Though it may not happen overnight, Gen Zers will likely make up the biggest share of homebuyers in the U.S. at some point, in the same way that millennials eventually became the dominant force in the housing market.

Tips for Gen Z homebuyers

Rising rates, high home prices and low housing inventory have made homebuying more difficult for many Gen Zers. But that doesn’t mean homebuying is an impossible goal for members of the generation.

Here are three tips that can help Gen Zers make the homebuying process more manageable:

- Boost your credit scores and savings. Because it’s a competitive seller’s market in many areas, would-be homebuyers need strong credit scores and substantial cash for a down payment to make a purchase. By focusing on paying down other debts before looking for a home to purchase, Gen Zers can boost their credit scores and free up extra cash that can go toward a home.

- Shop around for a mortgage. Shopping around for a mortgage before buying a home can help borrowers find a better mortgage rate, which can lower their monthly payments and help them figure out how much money they’ll qualify for and how expensive a house they’ll be able to afford.

- Consider first-time buyer programs. Various programs available to first-time homebuyers can make homeownership a more achievable goal for those with smaller down payments and lower credit scores. These programs are especially useful to Gen Zers, many of whom are first-time buyers.

Methodology

LendingTree used generational definitions from the Pew Research Center to define the age range for Gen Zers as being born between 1997 and 2012.

Metropolitan statistical area (MSA) rankings were generated by looking at the percentage of total purchase mortgage requests generated on the LendingTree platform from adult Gen Z borrowers (18 to 25) as a percentage of the total number of requests generated by borrowers of all ages. The larger the share of requests from Gen Zers, the higher ranking a metro received.

Borrower data was derived from mortgage purchase requests made by users of the LendingTree mortgage shopping platform across the nation’s 50 largest metros from Jan. 1 through Dec. 31, 2022.