Nearly 30% of Consumers in Largest Metros Opened at Least One Credit Card in First Half of 2023

Credit card interest rates are soaring — but that isn’t stopping consumers from opening new accounts.

According to the latest LendingTree study, 28.8% of consumers in the 100 most populous metros opened at least one credit card in the first six months of 2023.

Keep reading to learn who was most likely to open a new card and which metros had the highest percentage of credit card openings.

Key findings

- From Jan. 1 through June 30, 2023, 28.8% of consumers in the 100 most populous metros opened at least one credit card. The average credit limit for these newly opened cards was $5,011. Notably, 35.9% of millennials opened at least one card in this time frame — the highest by generation. And those with super-prime credit scores (720 and above) were the most likely credit score group to open a credit card, at 37.7%.

- Americans were most likely to open a credit card in the late spring. Across new credit cards opened from Jan. 1 through June 30, 21.8% of accounts were opened in May and 21.6% in June. Comparatively, just 11.1% of accounts were opened in January.

- Consumers were most likely to open credit cards in New Haven, Conn. 37.9% of residents in this metro opened at least one credit card from January through June. Deltona, Fla. (36.1%), and Colorado Springs, Colo. (33.7%), followed.

- Seven of the 10 metros where residents were most likely to open a credit card are in the South. Notably, six are in Florida. Of these 10 metros, Palm Bay, Fla., had the highest average credit limit among newly opened cards, at $6,042.

- Consumers in Milwaukee were least likely to open a new credit card in the first six months of 2023. Just 22.7% of residents here opened at least one account. Minneapolis and Salt Lake City consumers were second and third least likely, at 23.0% and 23.3%, respectively.

Nearly 30% of consumers in the 100 biggest metros opened a credit card in the first half of 2023

Across the 100 most populous metros in the U.S., 28.8% of consumers opened at least one credit card from Jan. 1 through June 30, 2023. On average, the credit limit for these cards was $5,011.

LendingTree chief credit analyst Matt Schulz says that the 28.8% figure is in line with what he’d expect.

By generation, millennials (ages 27 to 42) were the most likely to open a credit card in the first six months of the year, at 35.9%. That compares with:

- 35.1% of Gen Xers (ages 43 to 58)

- 20.6% of baby boomers (ages 59 to 77)

- 8.3% of Gen Zers (ages 18 to 26)

Of course, Schulz says, hitting certain milestones may contribute to the high percentage of millennials opening credit cards.

“With many millennials in their 30s or early 40s, their lives are crazy-expensive,” he says. “Sure, they’ve gotten a little more established in their careers and are likely earning a bit more these days, but they’re still wrestling with massive student loan debt, hanging on to hopes of maybe buying a house someday and managing the enormous costs of raising a family. That doesn’t leave much financial wiggle room, meaning that a lot of millennials need to look toward credit cards to extend their budget a bit and act as an emergency fund.”

In addition, those with super-prime credit scores of 720 and higher were the most likely to open a new card, at 37.7%. That compares with:

- 19.5% of consumers with prime credit scores (between 660 and 719)

- 16.6% of consumers with deep subprime credit scores (below 580)

- 14.1% of consumers with near-prime credit scores (between 620 and 659)

- 12.0% of consumers with subprime credit scores (between 580 and 619)

Notably, that means 28.6% of consumers in those 100 metros with subprime credit scores or lower opened a credit card in the first six months of the year — something Schulz attributes to the cost of living.

Schulz also believes that credit tightening might not have hit those with subprime credit as hard as other groups.

“There’s always a good amount of risk involved in lending to those consumers, so banks may not be as worried about lending to them because banks know what they’re getting into,” he says. “What we’re seeing now is that folks with really good credit and really bad credit are still able to get the cards they apply for, while those in the middle might be getting squeezed as banks get nervous about delinquencies and other signs of struggle among American consumers.”

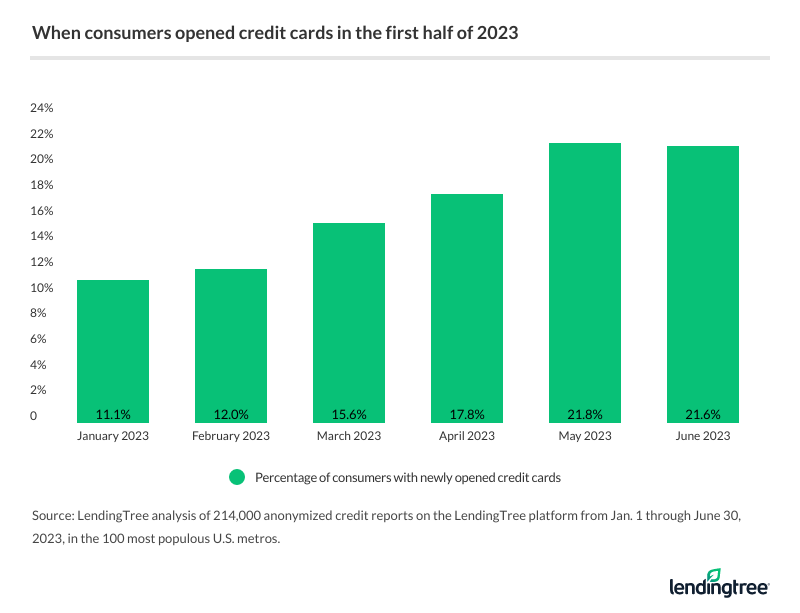

Americans were least likely to open a new credit card in January

Spring brings new beginnings — and credit cards are no exception. Across new credit cards opened from the beginning of January through the end of June, 21.8% of accounts were opened in May, making it the most likely month for consumers to open a new card. Following that, 21.6% were opened in June.

Meanwhile, January saw the lowest percentage of credit card openings in the months analyzed, at 11.1%.

Holiday debt and summer travel certainly go a long way to explaining the difference between credit card openings in May and June compared to January. However, Schulz believes that people are missing an opportunity by not applying for a new credit card at the beginning of the year.

“That’s because 0% balance transfer credit cards are maybe the best weapon people have in the battle against credit card debt,” he says. “It may seem counterintuitive and maybe even a little scary to get a new credit card when you already have debt, but a 0% balance transfer card, used wisely, can save you a small fortune in interest and dramatically reduce the time needed to pay off that balance.

37.9% of consumers in New Haven, Conn., opened a new credit card — here are the metros that followed

Consumers were most likely to open credit cards in a Constitution State metro — though another state dominated the top 10. From January through June 2023, 37.9% of New Haven, Conn., residents opened at least one credit card.

Following that, 36.1% of consumers in Deltona, Fla., and 33.7% of consumers in Colorado Springs, Colo., opened a new credit card during this period.

10 metros with the highest percentage of consumers who opened new credit cards

| Rank | Metro | % of consumers with newly open credit cards | Average credit limit |

|---|---|---|---|

| 1 | New Haven, CT | 37.9% | $4,520 |

| 2 | Deltona, FL | 36.1% | $4,507 |

| 3 | Colorado Springs, CO | 33.7% | $5,639 |

| 4 | Providence, RI | 33.2% | $5,146 |

| 4 | Orlando, FL | 33.2% | $4,853 |

| 6 | McAllen, TX | 33.1% | $3,501 |

| 7 | Tampa, FL | 32.8% | $5,032 |

| 8 | Miami, FL | 32.6% | $4,984 |

| 8 | Lakeland, FL | 32.6% | $4,143 |

| 10 | Palm Bay, FL | 32.4% | $6,042 |

Source: LendingTree analysis of 214,000 anonymized credit reports on the LendingTree platform from Jan. 1 through June 30, 2023, in the 100 most populous U.S. metros.

The South dominated the top 10 list, representing seven spots. Even further, six of the top 10 metros are in Florida. Of them, Palm Bay had the highest average credit limit among newly opened cards at $6,042.

Meanwhile, across all metros analyzed, newly opened credit cards in San Jose had the highest average credit limit at $7,550.

Milwaukee residents were least likely to open a new credit card

On the other end of the list, consumers in Milwaukee were least likely to open a new credit card. In the first six months of 2023, just 22.7% of Milwaukee residents opened at least one account. Minneapolis (23.0%) and Salt Lake City (23.3%) followed. Of the 10 metros with the lowest percentage of new credit card openings, it’s worth noting that five were in the West.

Of these metros, new credit cards in Seattle had the highest average credit card limit at $7,004 — the second-highest limit across all metros analyzed. Meanwhile, Wichita, Kan., had the lowest average credit card limit among the top 10 metros at $4,489.

Across all metros analyzed, newly opened credit cards in Winston-Salem, N.C., had the lowest average credit card limit at $3,188.

Full rankings: Where consumers were most likely to open a new credit card in the first half of 2023

| Rank | Metro | % of consumers with newly open credit cards | Average credit limit |

|---|---|---|---|

| 1 | New Haven, CT | 37.9% | $4,520 |

| 2 | Deltona, FL | 36.1% | $4,507 |

| 3 | Colorado Springs, CO | 33.7% | $5,639 |

| 4 | Providence, RI | 33.2% | $5,146 |

| 4 | Orlando, FL | 33.2% | $4,853 |

| 6 | McAllen, TX | 33.1% | $3,501 |

| 7 | Tampa, FL | 32.8% | $5,032 |

| 8 | Miami, FL | 32.6% | $4,984 |

| 8 | Lakeland, FL | 32.6% | $4,143 |

| 10 | Palm Bay, FL | 32.4% | $6,042 |

| 11 | Springfield, MA | 32.1% | $5,095 |

| 12 | Cape Coral, FL | 31.9% | $5,059 |

| 13 | Riverside, CA | 31.7% | $4,678 |

| 14 | Phoenix, AZ | 31.5% | $5,040 |

| 15 | San Antonio, TX | 31.4% | $3,952 |

| 16 | Harrisburg, PA | 31.1% | $4,949 |

| 17 | Bridgeport, CT | 30.9% | $5,803 |

| 17 | Chicago, IL | 30.9% | $5,090 |

| 19 | El Paso, TX | 30.8% | $3,851 |

| 19 | North Port, FL | 30.8% | $5,418 |

| 21 | Louisville, KY | 30.6% | $4,486 |

| 22 | Las Vegas, NV | 30.5% | $5,017 |

| 22 | Tulsa, OK | 30.5% | $3,921 |

| 22 | Bakersfield, CA | 30.5% | $4,147 |

| 25 | Baltimore, MD | 30.3% | $5,053 |

| 25 | Hartford, CT | 30.3% | $5,772 |

| 25 | Dallas, TX | 30.3% | $4,893 |

| 28 | Richmond, VA | 30.2% | $4,773 |

| 28 | Worcester, MA | 30.2% | $4,909 |

| 30 | Jacksonville, FL | 30.1% | $5,288 |

| 31 | Virginia Beach, VA | 30.0% | $4,606 |

| 32 | Atlanta, GA | 29.9% | $5,101 |

| 33 | Greensboro, NC | 29.8% | $3,305 |

| 34 | Oxnard, CA | 29.8% | $6,296 |

| 35 | Los Angeles, CA | 29.7% | $5,493 |

| 35 | Tucson, AZ | 29.7% | $4,664 |

| 37 | Syracuse, NY | 29.4% | $4,820 |

| 37 | Little Rock, AR | 29.4% | $4,397 |

| 39 | Allentown, PA | 29.3% | $4,122 |

| 39 | Stockton, CA | 29.3% | $5,215 |

| 41 | San Jose, CA | 29.2% | $7,550 |

| 42 | St. Louis, MO | 29.1% | $5,184 |

| 43 | Detroit, MI | 29.0% | $5,105 |

| 43 | Indianapolis, IN | 29.0% | $5,092 |

| 45 | Boston, MA | 28.9% | $6,027 |

| 46 | Denver, CO | 28.8% | $6,128 |

| 47 | Ogden, UT | 28.7% | $5,209 |

| 48 | Nashville, TN | 28.6% | $5,176 |

| 48 | Augusta, GA | 28.6% | $3,624 |

| 48 | Birmingham, AL | 28.6% | $4,205 |

| 48 | New York, NY | 28.6% | $5,202 |

| 48 | Poughkeepsie, NY | 28.6% | $5,154 |

| 48 | Sacramento, CA | 28.6% | $5,473 |

| 54 | San Diego, CA | 28.5% | $6,473 |

| 54 | Winston-Salem, NC | 28.5% | $3,188 |

| 56 | Raleigh, NC | 28.2% | $4,386 |

| 56 | Fayetteville, AR | 28.2% | $4,793 |

| 58 | Knoxville, TN | 28.1% | $4,523 |

| 58 | Honolulu, HI | 28.1% | $6,247 |

| 58 | Toledo, OH | 28.1% | $4,908 |

| 61 | New Orleans, LA | 28.0% | $3,622 |

| 61 | Columbia, SC | 28.0% | $3,937 |

| 63 | Durham, NC | 27.8% | $4,621 |

| 63 | Austin, TX | 27.8% | $5,720 |

| 63 | Buffalo, NY | 27.8% | $4,780 |

| 66 | Albuquerque, NM | 27.6% | $4,786 |

| 66 | Akron, OH | 27.6% | $4,818 |

| 66 | Dayton, OH | 27.6% | $3,938 |

| 69 | Cleveland, OH | 27.5% | $4,279 |

| 70 | Houston, TX | 27.4% | $5,325 |

| 70 | Jackson, MS | 27.4% | $3,380 |

| 70 | Rochester, NY | 27.4% | $5,254 |

| 73 | Pittsburgh, PA | 27.3% | $5,247 |

| 73 | Philadelphia, PA | 27.3% | $5,434 |

| 75 | Fresno, CA | 27.2% | $3,605 |

| 75 | Omaha, NE | 27.2% | $5,912 |

| 75 | Baton Rouge, LA | 27.2% | $3,902 |

| 78 | Grand Rapids, MI | 27.1% | $4,564 |

| 79 | Columbus, OH | 26.9% | $5,041 |

| 80 | Charleston, SC | 26.8% | $5,539 |

| 80 | Albany, NY | 26.8% | $4,619 |

| 80 | Des Moines, IA | 26.8% | $5,329 |

| 83 | Cincinnati, OH | 26.6% | $5,036 |

| 84 | Kansas City, MO | 26.5% | $5,298 |

| 84 | Oklahoma City, OK | 26.5% | $5,051 |

| 86 | Boise, ID | 26.4% | $5,841 |

| 86 | Memphis, TN | 26.4% | $3,615 |

| 88 | Washington, DC | 26.3% | $6,059 |

| 88 | San Francisco, CA | 26.3% | $6,973 |

| 90 | Greenville, SC | 25.9% | $4,540 |

| 91 | Wichita, KS | 25.6% | $4,489 |

| 92 | Spokane, WA | 25.4% | $4,656 |

| 93 | Seattle, WA | 25.3% | $7,004 |

| 94 | Portland, OR | 24.8% | $5,403 |

| 95 | Provo, UT | 24.3% | $6,969 |

| 96 | Madison, WI | 24.0% | $5,836 |

| 97 | Charlotte, NC | 23.7% | $5,693 |

| 98 | Salt Lake City, UT | 23.3% | $6,361 |

| 99 | Minneapolis, MN | 23.0% | $5,939 |

| 100 | Milwaukee, WI | 22.7% | $5,454 |

Source: LendingTree analysis of 214,000 anonymized credit reports on the LendingTree platform from Jan. 1 through June 30, 2023, in the 100 most populous U.S. metros.

Opening a new card? Here’s what experts recommend

Navigating today’s sky-high interest rates can feel overwhelming when applying for a new credit card — particularly if your credit score needs work. For those looking to open a new card, here’s what Schulz recommends:

- Shop around. “There are so many different types of cards, and the offers can vary widely when it comes to rewards, fees, rates and more,” he says. “Take the time to compare cards at sites like LendingTree or by checking out issuers’ websites and make sure that you’ve found the card that’s the best fit for you.”

- Consider a secured credit card. “If you have thin or poor credit, a secured credit card can be a great tool to help you build credit,” Schulz says. “It works just like any other credit card, except you have to put down a deposit to establish the credit limit. That means the limits are typically pretty small, but the card can still be a good stepping stone card for a year or so until you’re ready for a regular credit card.”

- Don’t close your other cards just because you’re getting a new one. “It can be tempting to want to be rid of your old credit cards when you sign up for a new one, but that can damage your credit,” he says. “Your best move is likely to keep the card open and use it occasionally to keep it active.” Consider putting a small recurring subscription, like a Spotify membership, on the card and auto-paying it every month. That way, the card stays active but you don’t have to worry about running up any new debts. Unless the card has a big annual fee, leaving it open is usually the way to go.

Methodology

To determine the percentage of consumers who’ve opened a new credit card, LendingTree researchers analyzed a sample of 214,000 anonymized credit reports from Jan. 1 through June 30, 2023, in the 100 most populous U.S. metros.

Researchers used the U.S. Census Bureau 2022 American Community Survey with one-year estimates to identify the 100 largest metros.

Analysts then divided the number of consumers who opened at least one credit card in that period by the total number of consumers with a credit report. The study considered individual and joint accounts, with joint accounts counting for half to avoid duplication.

The content above is not provided by any issuer. Any opinions expressed are those of LendingTree alone and have not been reviewed, approved, or otherwise endorsed by any issuer. The offers and/or promotions mentioned above may have changed, expired, or are no longer available. Check the issuer's website for more details.