Foreign Transaction Fee: What is it? How does it work?

If you’ve used your credit card outside of the U.S., you’ve no doubt come across foreign transaction (FX) fees — fees of around 3% charged by banks on purchases made overseas. These pesky little charges are often buried deep in the terms and conditions of your credit card agreement. You may be wondering: What exactly are these transaction fees? Are they always the same? And are there cards that don’t charge foreign transaction fees?

We’ve researched and assembled this guide to help consumers find answers to these questions, and better understand foreign transaction fees and how they work.

On this page

- What is a foreign transaction fee?

- How are foreign transaction fees calculated?

- Which credit cards have no foreign transaction fees?

- How to spot credit card foreign transaction fees

- When are foreign transaction fees charged?

- How to avoid foreign transaction fees

- Do FX fees count when earning credit card rewards?

- Conversion charges: Charges in USD vs. local currency

- FAQs

What is a foreign transaction fee?

A foreign transaction (FX) fee is a surcharge on your credit card bill that appears when you make a purchase that either passes through a foreign bank or is in a currency other than the U.S. dollar (USD). This fee is charged by many credit card issuers, typically ranging from 1% to 3% of the transaction.

The foreign transaction fee consists of two parts:

- Network fee (or currency conversion fee): This part of the FX fee is charged by the credit card network (Visa or Mastercard, for example). Visa and Mastercard both charge a fee of 1%. Regardless of the type of credit card, this fee is applied to all transactions.

- Issuing bank fee: Depending on the credit card you use — such as Citibank, Chase or Barclays — some issuers add a charge on top of the network fee, usually around 2%. Other issuers don’t add their own and even go as far as absorbing the network fee, so you won’t have to pay anything.

Even though there are two parts to the fee, foreign transaction fees are typically assessed as a single charge to your credit card statement per purchase. Card issuers decide whether and how these fees are assessed.

How are foreign transaction fees calculated?

Imagine you pay €93 while on vacation in Spain, using a card on the Mastercard network that has a 2% issuing bank fee. With the currency conversion, this works out to $100 in USD.

Based on that converted amount, Mastercard will charge 1% on top of the cost of your room. Then, the issuer will charge another 2% on top of that.

Therefore, the actual cost of your hotel comes out to be ($100 * (1% + 2%)) + $100 = $103. This might not seem like much, but an extra 3% on top of all your vacation expenses can quickly add up.

Remember that exchange rates factor in when dealing with most foreign transactions. Being charged €20 for lunch doesn’t mean your credit card will be charged $20. The charge will be converted to dollars using the current exchange rate. Both Mastercard and Visa calculate exchange rates to convert all foreign-denominated transactions to USD. Foreign transaction fees are charged based on the USD transaction after currency conversion has taken place.

Some merchants will ask if you want to be charged in USD upfront, through a process called dynamic currency conversion — we advise against this. It may seem helpful to know the total cost in USD; however, dynamic currency conversion typically comes with an unfavorable exchange rate.

Which credit cards have no foreign transaction fees?

There are many credit cards that waive foreign transaction fees as a benefit, and most of these are travel credit cards. Many co-branded hotel and airline cards carry no foreign transaction fees, while premium travel rewards cards (i.e., travel rewards cards with high annual fees) also typically don’t charge foreign transaction fees.

Cards with no annual fees or foreign transaction fees are more rare, but there are at least a handful on the market (including the Capital One VentureOne Rewards Credit Card below).

Top credit cards with no foreign transaction fee

| Recommended card | Earning rate | Annual fee |

|---|---|---|

| Chase Sapphire Preferred® Card | Enjoy benefits such as 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases | $95 |

| Capital One Venture Rewards Credit Card | 2 Miles per dollar on every purchase, every day; 5 Miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel | $95 |

| Capital One VentureOne Rewards Credit Card | 1.25 Miles per dollar on every purchase, every day; 5 Miles per dollar on hotels, vacation rentals and rental cars booked through Capital One Travel | $0 |

Beyond our top picks, there are many more cards without FX fees, which we’ve highlighted in the table in the next section. Alternatively, check out some of the best credit cards for international travel, none of which charge foreign transaction fees.

Foreign transaction fees by credit card issuer

Foreign transaction fees vary by card issuer. This rate can even vary between card products from the same issuer. The table below provides both the typical FX fee by issuer, plus a selection of the cards without FX fees offered by that bank. Every major bank offers at least one card without foreign transaction fees.

| Issuer | Typical FX Fee | No-Foreign-Transaction-Fee Credit Cards (samples) |

|---|---|---|

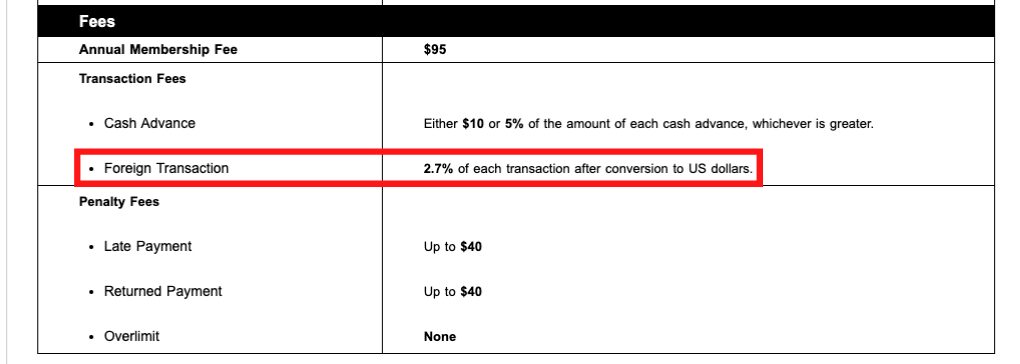

| American Express | 2.70% | '

|

| Bank of America | 3% | ' |

| Barclays | 3% | '

|

| Capital One | 0% | '

|

| Chase | 3% | '

|

| Citibank | 3% | '

|

| US Bank | Up to 3% | '

|

Capital One and Discover are unique in that they don’t levy foreign transaction fees on any card products

As far as the other issuers go, the foreign transaction fee is typically around 3%, when levied. Still, there are plenty of cards that don’t assess international transaction fees, so you should be able to easily avoid them.

How to spot credit card foreign transaction fees

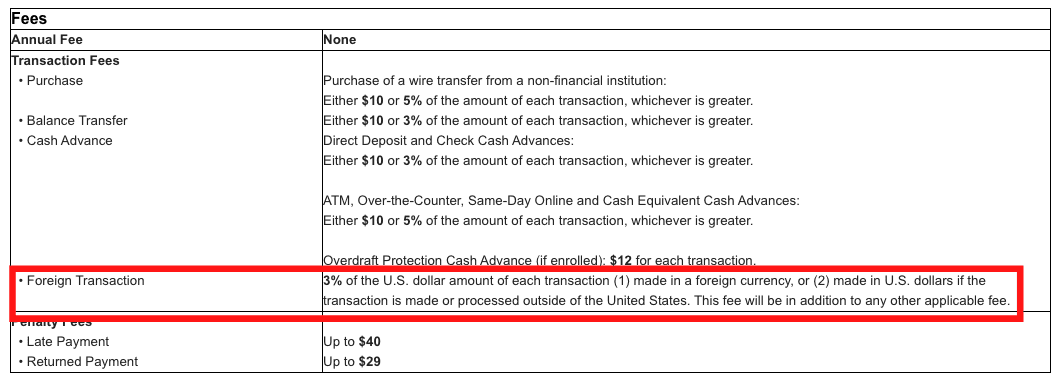

Issuers typically don’t advertise the fact that their cards charge foreign transaction fees unless a product lacks these fees. If you don’t see “no foreign transaction fees” advertised as a benefit for a card product, you can typically assume the card will charge an FX fee. To be certain, check the terms and conditions (sometimes called “Pricing and Terms” or “Rates and Fees”) for your particular card. The foreign transaction fee will be listed under the “Fees” section, alongside the card’s annual fee and other fees, such as cash advance and penalty fees.

When are foreign transaction fees charged?

Credit card networks flag transactions as “foreign” if, at any point, the transactions pass through a foreign bank. You don’t necessarily have to be located outside the U.S. at the time of purchase. Some purchases, such as online purchases from foreign merchants shown in foreign currency, will incur foreign transaction fees. Even if your transaction is executed in USD, it may incur an FX fee if it’s routed through a foreign bank.

You could be charged a foreign transaction fee if:

- A purchase occurs from a merchant located outside the U.S.

- A purchase is in a foreign currency

- A purchase is routed through a foreign bank (sometimes even when it’s charged in U.S. dollars)

Keep in mind that even if a purchase appears to be charged in U.S. dollars, this doesn’t mean it won’t incur a foreign transaction fee. Some countries, such as Panama and Ecuador, use the U.S. dollar as their currency.

How to avoid foreign transaction fees

Foreign transaction fees can be annoying, but there are easy ways to avoid them before and after you travel abroad.

- Get a credit card that doesn’t have a foreign transaction fee. If you’re a frequent traveler, this is a savvy investment. If you invest in a travel card with an annual fee, then you likely won’t have to deal with foreign transaction fees. But there are no annual fee cards with no FX fees, too, like the Bank of America® Travel Rewards credit card and the Wells Fargo Autograph® Card.

- Get a debit card that doesn’t charge foreign transaction fees, either.You can use your debit card for getting money in a different currency at an ATM. However, like credit cards, they can come with extra foreign fees — so opt for a debit card that doesn’t have those so you’ll only have to pay the required exchange rate.

- Use an ATM card that reimburses ATM fees.It’s usually wise to have local cash on hand when traveling in a foreign country. However, you can incur both international transaction fees and out-of-network ATM fees when withdrawing cash outside the U.S. Make sure that you use an ATM card that reimburses ATM fees. Some ATMs also try to hit you with DCC, so avoid that as well. This ensures you’ll receive the wholesale currency exchange rate that day.

Do FX fees count when earning credit card rewards?

Sadly, foreign transaction fees don’t count toward rewards spending. In the example above where we spent $100 on lodging using a cash back card, cash back would only be earned on the $100 bill, not on the final $103 cost — banks charge the fee separately on your bill. Just like with interest, annual fees and late fees, you won’t earn any rewards for foreign transaction fees. Rewards for general-purpose credit cards tend to hover around the 1.5% to 2% level, so a 3% FX fee would erase any rewards earned.

Conversion charges: Charges in USD vs. local currency

Sometimes when you’re traveling abroad, a merchant may give you the option to convert your charges to USD instead of the local currency, in a process called dynamic currency conversion (DCC). We advise against choosing DCC, as you’ll almost always end up paying more.

The problem is that DCC nearly always results in unfavorable exchange rates. When a merchant processes your payment using DCC, they get to set the currency exchange rate, and this can add as much as an additional 7%, or possibly even more, to the transaction. Merchants are incentivized to pick an unfavorable rate, as this pads their profits as well as those of the third-party DCC service provider. To avoid being overcharged, choose to pay in the local currency instead. The currency conversion will be handled automatically by your credit card network using their exchange rate.

To add insult to injury, you may still end up getting charged a foreign exchange fee even if you use dynamic currency conversion and the transaction is performed in USD. All that needs to happen is for the transaction to pass through a foreign bank. Sometimes a card issuer specifically spells out how this is handled. The terms and conditions may specify if there’s a fee for foreign transactions in U.S. dollars versus local currency.

If your card issuer only specifies local currency fees, this means they don’t charge for transactions in USD. Due to the Truth in Lending Act, credit issuers in the U.S. are required to disclose all fees in the terms and conditions.

Even if your issuer doesn’t charge for transactions in USD, avoid using DCC. The exchange rate chosen by the merchant almost always increases the total cost. Make sure the total on your receipt shows the charge in local currency.

Frequently asked questions

Foreign transaction fees vary, but they’re typically around 3% when levied by a card issuer.

Like any other fee, banks charge foreign transaction fees in order to make money off of credit card usage by consumers.

Foreign transaction fees are issued by the lender and can be deducted like any other credit card fee as a business expense, as long as the purchase itself was made for business purposes.

Many debit cards have foreign transaction fees. You’ll need to check the terms and conditions of your card agreement to determine whether your bank charges these fees.

Yes, foreign transaction fees can apply to online purchases in a foreign currency or where a transaction is routed through a foreign bank.

To determine a foreign transaction fee, first check your card agreement to determine the fee percentage. Then, if the charge isn’t in USD, you’ll need to check the network calculator for the specific date of the transaction to calculate the conversion to USD (Both Visa and Mastercard provide one. Apply the foreign transaction fee percentage to the total once converted to USD to determine the total fee.

No, many cards waive foreign transaction fees as a benefit. See our table in the article above for cards that don’t charge foreign transaction fees.

You’ll need to check your card agreement to determine whether your card charges a foreign transaction fee. Find the agreement provided with your card, if you have it filed somewhere. Alternatively, you can find your card online and check the “Pricing and Terms” or “Rates and Fees” for the card. Look under the fees section to determine whether your card charges a foreign transaction fee.

To see rates & fees for American Express cards mentioned on this page, visit the links provided below:

- Hilton Honors American Express Surpass® Card

- American Express Platinum Card®

- Delta SkyMiles® Reserve American Express Card

- Delta SkyMiles® Platinum American Express Card

- Marriott Bonvoy Brilliant® American Express® Card

For Capital One products listed on this page, some of the benefits may be provided by Visa® or Mastercard® and may vary by product. See the respective Guide to Benefits for details, as terms and exclusions apply

The information related to the Hilton Honors Aspire Card from American Express, AtmosTM Rewards Ascent Visa Signature® credit card, Hawaiian Airlines® Business MasterCard®, AAdvantage® Aviator® Red World Elite Mastercard®, JetBlue Business Card, Chase Sapphire Reserve®, The New United℠ Explorer Card, The New United Club℠ Card, British Airways Visa Signature® Card, Southwest Rapid Rewards® Premier Credit Card, IHG One Rewards Premier Credit Card, World of Hyatt Credit Card, Marriott Bonvoy Boundless® Credit Card, Citi® / AAdvantage® Executive World Elite Mastercard®, Costco Anywhere Visa® Card by Citi, U.S. Bank Altitude® Go Visa Signature® Card, U.S. Bank Altitude® Connect Visa Signature® Card and Wells Fargo Autograph® Card has been independently collected by LendingTree and has not been reviewed or provided by the issuer of this card prior to publication. Terms apply.

The content above is not provided by any issuer. Any opinions expressed are those of LendingTree alone and have not been reviewed, approved, or otherwise endorsed by any issuer. The offers and/or promotions mentioned above may have changed, expired, or are no longer available. Check the issuer's website for more details.